If you have been watching the 2024 European Championship in Germany, you may have noticed the number of Chinese sponsors present.

Among the companies representing Chinese tech, Alibaba’s online payment app Alipay could be seen on billboards during the games.

Alipay is one of China’s most popular payment apps, and many believe it and other similar Chinese payment methods are more convenient than what’s available in the West.

Online Payments in China

When we last tackled this subject in 2017, China was attempting to move towards a cashless society as it gradually got rid of services that only allowed paper money.

Seven years later, the initiative has run into issues, particularly with visiting tourists and how they spend their money in China.

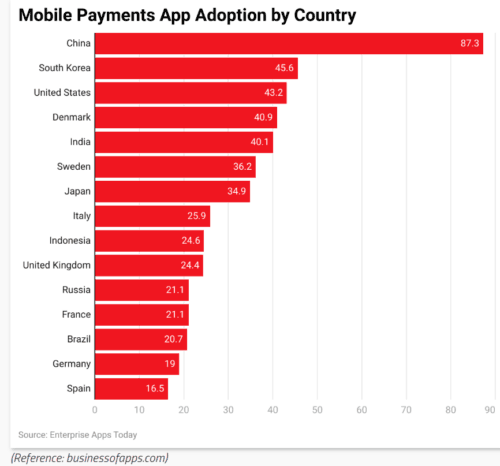

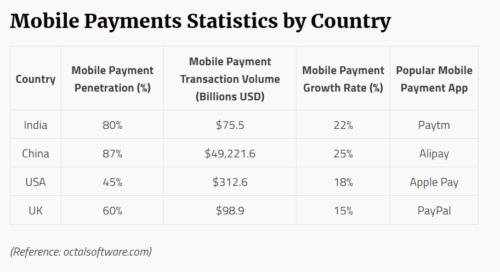

Nevertheless, the country is still far ahead in integrating online payment mechanisms than most other countries. The below charts are for 2024.

But why is China pursuing this?

Like other countries, moves to get rid of paper money are seen as a way to reduce crime. Although China’s opening up to the world in the 1980s allowed it to become the economic behemoth it is today, the past decades saw a rise in crime.

This has decreased over the past 10 years, possibly due to the evolution of online payments.

Unlike paper money, electronic payments can be tracked, and while a thief can steal a person’s phone from their pocket (like a wallet), they still need a password or fingerprint to unlock the device.

Besides safety, Chinese citizens love convenience.

With mobile payment apps, people can now ditch the physical wallet and free up some pocket space.

Growth of Online Payments in China

As of 2024, a little under 900 million people in the country use their phones to make purchases. As for the remaining 500 million people, perhaps their family members help them make online purchases.

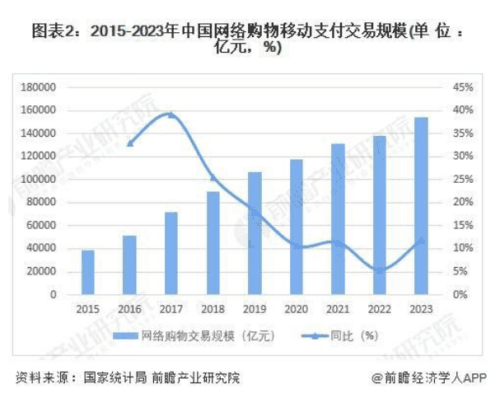

In 2023, over 2 trillion dollars in payments were made online in China, and the chart below shows the growth of online payments in Chinese Yuan over the past decade.

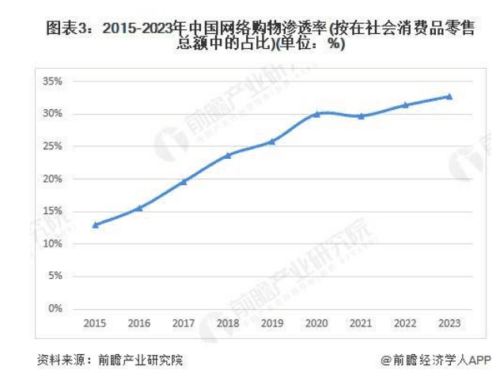

Growth can also be seen in the percentage of payments processed online.

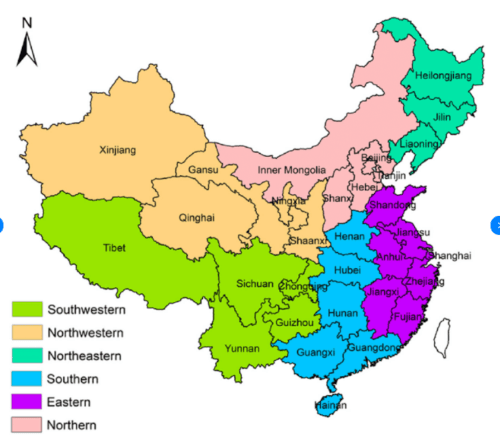

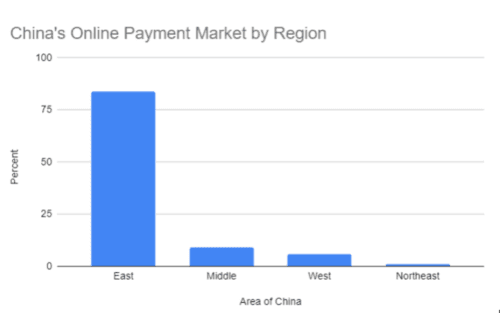

China’s online payments market can be broken down by economic region.

Notice how there is no “south.”

Guandong’s (the province with Shenzhen in blue) development has been much more similar to the other coastal regions in China compared to the other southern provinces of Yunnan (the green province with Kunming in green) and Guangxi (the green province with Nanning).

Northeast China (orange) is a separate section due to its history as an industrial region during Japanese rule. Today, it is economically behind the other coastal regions and is considered a rust belt.

As you can tell from the above chart, the coasts dominate e-commerce, which can be attributed to their role in the Chinese economy since the country opened up in the 1980s.

The richest cities and the best universities are also here.

These areas are also more international, and many young people have migrated to these regions; since the 1990s, Guangdong has replaced Henan as China’s most populous province.

If we break down this chart, east China controls 83.92% of the market while Middle China and West China control 8.87% and 5.73%, respectively. Northeast China has only 1.48%.

Given this data, online payments have taken China by storm over the past decade!

China’s Online Payment Companies: Two Tiers

Being a big country with some provinces more developed than others, the landscape for online payment companies is quite diverse too, and these companies can be divided into two tiers.

The higher tier of online payment companies is Alibaba’s Alipay (支付宝), Tencent’s WeChat Pay (财付通) and UnionPay.

The second tier is made up of a bunch of other competitors.

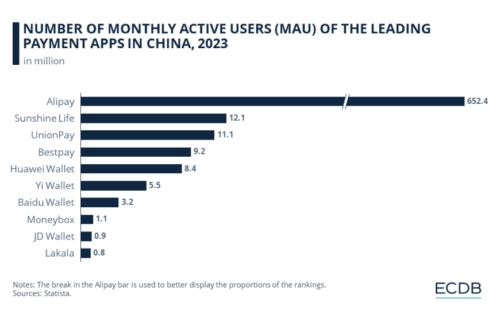

This chart shows the results of a survey showing how many people used these online payment methods in the past year.

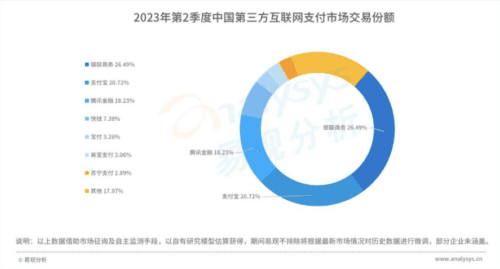

Keep in mind, however, that not every review of China’s online payment market is the same.

For example, another source shows UnionPay has the highest share of transactions (26%), with Alipay (21%) and Tencent Pay (18%) rounding out the top three.

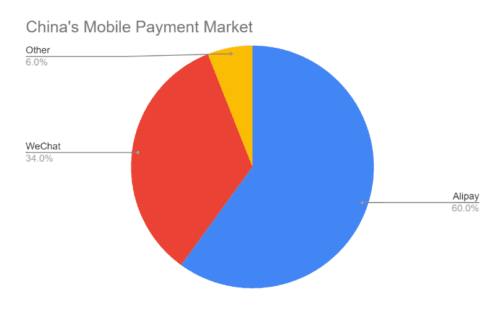

Another source shows Alipay and WeChat Pay control more than 94% of the overall market for mobile payments, with Alipay (支付宝) being the leader. Note that mobile payments are online, but not all online payments are mobile. In Q3 2023, the transaction volumes of Alipay and WeChat Pay were 118.19 trillion yuan and 67.81 trillion yuan respectively.

I will go over the top-ranked payment options in China according to Chinaapp first. However, as already noted, please know that not every website has the same ranking. Over the course of this article, I will go over every payment method mentioned across different articles.

Foreign Travelers

One issue China has faced since going more cashless is that the apps used within the country aren’t the same as cash apps used in other countries, even in the rest of East Asia.

This has posed challenges to foreign tourists and older Chinese citizens.

For the former, the biggest problem has been that China’s mobile banking apps have required a Chinese bank account, and tourists don’t want to have their bank accounts directly linked to a Chinese app in China.

Those unwilling to use Chinese apps might be refused service because a business may not accept paper money.

In recent months, moves have been made to simplify everything for foreigners. For example, tourists no longer need to register their ID on Alipay (as long as they spend less than $2000 a year on the app).

China’s Top Three Online Payment Apps – Alipay, WeChat Pay, and UnionPay

There are a number of apps in China for making online payments.

This article will address these from most to least popular, but I have separated the discussion into three sections.

This section will focus on the three biggest apps.

Alipay (支付宝)

Alipay is a part of the Alibaba Group and is the most-used online payment platform in China—accepted by 80 million businesses and used by over 1 billion users.

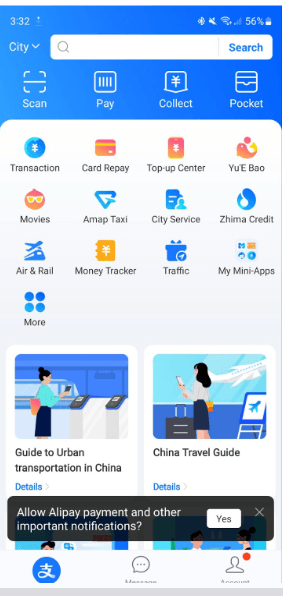

Like WeChat, Alipay’s success and popularity do not merely hinge on its online payment prowess but rather on the range of other features it offers to users:

- Taxi hire

- Hotel bookings

- Bicycle rental

- And more

Internationally, Alipay operates in more than 110 countries and has partnered with over 250 overseas financial institutions, and this has been fueled by the growth of Chinese tourists going abroad.

Another reason Alipay has been successful is its integration with Alibaba’s other products – Tmall and Taobao.

Although these platforms are not as dominant as they used to be, the two together have a 50.8% share of China’s e-commerce market.

How Does Alipay Work?

Users can attach a bank account to Alipay or keep money on the app separate from their bank.

Alipay deducts payment from the buyer’s Alipay account in real-time in CNY and settles the payment to your account in a chosen currency.

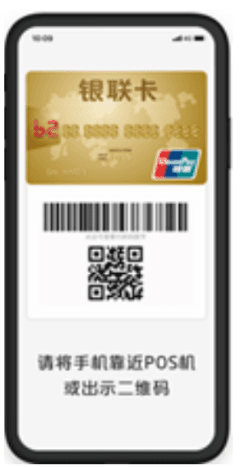

Users can pay other people by scanning a QR code or adding them as a friend.

Transaction Information Within China

Alipay Card Transaction Limit: 5000 RMB per

- transaction,

- day,

- month

- year (by natural year)

Transfer Limit to a Bank Card:

- RMB 50,000 per transaction

- RMB 20,000 per day

- RMB 200,000 per month (excluding service charge)

NOTE: Transfers to other Alipay apps are free!

Business Account Transfer to Another Account:

- Single transfer limit: For transfers to individual Alipay accounts, the maximum amount for a single transfer is 50,000 yuan; for transfers to business Alipay accounts, the maximum amount for a single transfer is 100,000 yuan.

- Daily limit: the initial amount is 2 million yuan, i.e., the maximum daily transfer is 2 million yuan.

- Monthly limit: The initial amount is 31 million yuan, i.e., the maximum monthly transfer of 31 million yuan.

- The above Alipay transaction limit will be adjusted according to the actual transfer of funds.

- Supported currencies: GBP, HKD, USD, SGD, JPY, CAD, AUD, EUR, NZD, KRW, THB, CHF, SEK, DKK, NOK, MYR, IDR, PHP, MUR, ILS, LKR, RUB, AED, CZK, ZAR, CNY.

For more information about Alipay internationally, please see this article, and for more information on transactions, visit here.

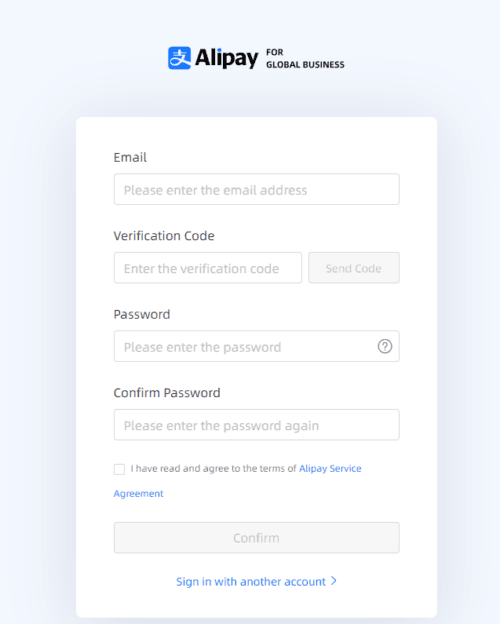

How to Set Up an Alipay Account

Method One → Alipay’s Website

Head over to Alipay Global’s website and fill out the following information.

Once you have submitted your company’s information for verification, you’ll need to wait 5–7 business days.

Companies should have an authentic and updated business license in their home countries.

For more information on how to accept payments for both Alipay, please see our 2022 article here.

Method Two → Use Stripe

For a shortcut, enable Alipay via Stripe.

This means you do not need to create your own Alipay account.

WeChat Pay

WeChat Pay belongs to the tech company Tencent, and its payment business is sometimes called Tenpay or Caifutong (财付通).

However, I will refer to it by its more well-known name: WeChat Pay.

When NMG tackled the topic of online payments back in 2017, WeChat Pay had only been around for about a year.

As of 2023, the service has 1.133 billion users.

The main reason for WeChat Pay’s growth over the years is its incorporation into the app’s chat tool, many users prefer to use WeChat Pay over Alipay because WeChat is their main social messaging application, and users can send money to their contacts within the messaging window.

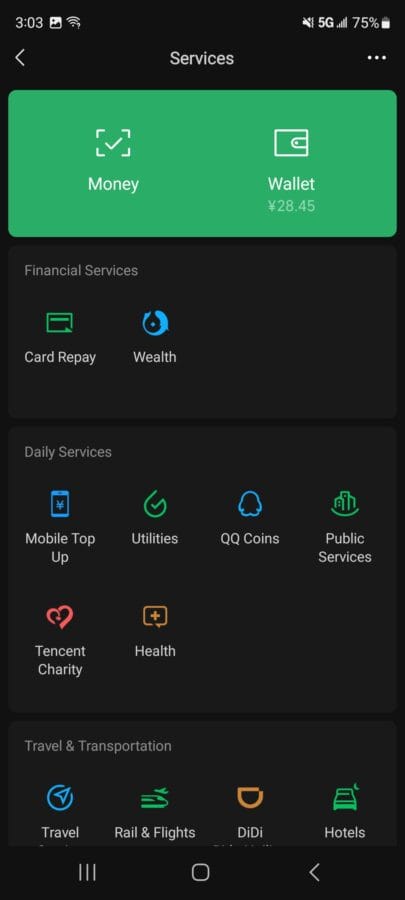

As you can see in the image above, WeChat Pay, like Alipay, allows users to pay for several different services.

How Does WeChat Pay Work?

Six ways WeChat users can pay:

- Quick Pay: Each user has a unique QR code associated with their WeChat account. To pay, a customer just needs to show this code to a shopkeeper for them to scan it.

- Scan: This is the opposite of Quick Pay. For this, a user scans the QR code belonging to the shopkeeper.

- Mini-Programs: Mini-Programs are apps within WeChat, and companies can set them up. Just like with normal apps, a user may choose to make a purchase.

- Official Accounts: If a company chooses not to make a mini-program, they may select an Official Account instead. These are similar to Facebook pages except they also send users notifications. You can learn more about mini-programs and Official Accounts here.

- In-App Payment: Companies can also integrate WeChat into their own apps.

- Web Payment: The user scans a QR code on a website.

Alipay, like WeChat Pay, deducts the payment from the buyer’s account in real-time in CNY and settles the payment to your account in a chosen currency.

Transaction Information

WeChat Pay settles each transaction with foreign vendors based on the price in local currency. For unsupported currencies, transactions can be in US dollars.

- Major Currencies Allowed: HKD, USD, GBP, JPY, CAD, AUD, EUR, NZD, KRW, THB, SGD, RUB, DKK, SEK, CHF and NOK.

For the transaction rules, please see WeChat’s site here.

How to Set Up a WeChat Business Account

Method One → Through WeChat

- Validate Your Business: Like Alipay, companies must provide paperwork to prove they are registered in their home countries.

- Set up a Bank Account: Make sure the name registered to your bank account matches the name on your registration papers.

- Link Bank Account With WeChat: Link the above bank account with your WeChat Account.

- Match Payment Systems: Ensure your company’s payment system can work with WeChat. If not, we can help you find developers to fix any bugs.

- Classify Business Correctly: To categorize and facilitate transactions, every business is assigned a merchant category code to classify its goods or services.

- Understand China’s Tax System: WeChat also requires businesses to have a system in place so that any transactions can be easily taxed yearly.

- Customer Support: Companies are also required to have a customer support system to manage their business transactions.

- Understand Market and Sector Restrictions: China has laws concerning its market and different industries, and companies should have people capable of understanding these.

- International Currencies: Your transaction system should handle currency conversions and settlements.

You can read more on how to accept payments for both WeChat here.

Method Two → Use Stripe

As with Alipay, it’s often possible to enable WeChat Pay payments on your website via Stripe, and this means you do not need to create your own WeChat Pay account.

UnionPay

Internationally known UnionPay known as UnionPay International, UnionPay is the largest state-owned financial services institution in China and plays an important role in its home country.

A few decades ago, Chinese citizens had trouble using cards in different regions of the country, and UnionPay’s card system changed this.

UnionPay’s cards can be used in 181 countries and regions worldwide, and while UnionPay has surpassed Visa and Mastercard in terms of card payments internationally, only 0.5% of its payments occur outside of China.

Over the past decade, the company has expanded its relations with foreign companies to help Chinese manage their money abroad.

For payments using UnionPay to be made outside of China, a third-party service is required:

Overseas, UnionPay International has also partnered with Huawei Pay and Apple Pay.

Huawei Pay

Although Huawei has had some issues in North America, it has still broken a lot of ground in other parts of the world, and Huawei Pay can be used in several countries including

- Russia,

- Hong Kong,

- Macao,

- Pakistan,

- Thailand,

- Singapore,

- and Malaysia.

Huawei’s cooperation with UnionPay makes it easy for people to use money from their bank accounts back in China.

Apple Pay

While Apple Pay is building steam in the United States with more and more people adopting its mobile payments services every year since its release in 2014, Chinese abroad are using its services too.

UnionPay has partnered with Apple Pay to help Chinese cardholders in Hong Kong and Macao.

How Does UnionPay Work?

UnionPay’s core services can be broken down further into three institutions.

Let’s go over them one by one in terms of popularity.

Quick Pass 闪付

Quick Pass is UnionPay’s most popular online payment service.

Released in 2017, Quick Pass allows Chinese users to connect their UnionPay card to their phones for payment and, like Alipay and WeChat, the app relies on QR codes and contactless payments.

Although Quick Pass was far behind the other two in the first few years of app payments, it has caught on more since 2021 when the government stepped in to end Alipay and WeChat’s monopoly on the industry.

UnionPay’s connection to the government should not be underestimated as it is unlikely that the app would be allowed to end as a service.

The company has a 45% share of the global market for card spending, which is more than Mastercard and Visa, and they have also partnered with Discover in the US.

Worldwide, there are over 9.4 billion UnionPay cards in circulation (mostly in China) and 200 million internationally.

QuickPass is in third place, just as it was in 2022.

Like WeChat and AliPay, Quick Pass enables contactless payments.

This service is supported on several portable devices, even smartwatches.

ChinaUMS (银联商务)

Founded in 2002, China UMS or China UnionPay Merchant Services Co., Ltd is also run by UnionPay and is now ranked fourth in terms of online payments in China (sitting in sixth place just two years earlier).

According to their website, they were “one of the first payment institutions to obtain the Payment Business License issued by the People’s Bank of China.”

China UMS has also been expanding its reach internationally.

In 2017, the Japanese payment settlement agency Merchant Support Co., Limited became their wholly-owned subsidiary to help Chinese tourists pay when visiting their East Asian neighbors.

UnionPay Online (银联在线) (Also known as ChinaPay)

As the last of the services offered by UnionPay, UnionPay Online is a platform that allows users to make online transactions with all types of UnionPay cards.

Backed by the government, UnionPay Online is known for being a secure, fast, and global payment experience for

- domestic and international online shopping,

- utility bill payments,

- travel bookings,

- transfers,

- fund subscriptions,

- charitable donations, and

- business collections and payments.

Some of UnionPay Online’s standout features include

- convenience,

- security,

- worldwide acceptance,

- financial-grade transaction guarantees,

- comprehensive merchant services, and

- easy online access without the need for bank account linkage.

UnionPay’s extensive global network allows cardholders to shop worldwide with a click; however, UnionPay Online appears to have moved from fifth to fourth place in 2022.

It should be noted that not all websites seem to classify all UnionPay’s services as separate entities.

How to Set Up a UnionPay Business Account

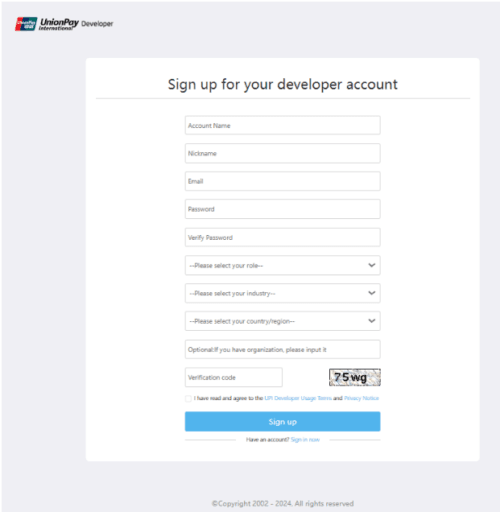

Method One → UnionPay International’s Website

Businesses interested in using UnionPay’s online payment services can go to their website. Once there, they will be greeted by the following screen.

If you tap on “Register Now” under the “UnionPay International Developer” title, you’ll be taken to the following screen where you can supply the necessary information:

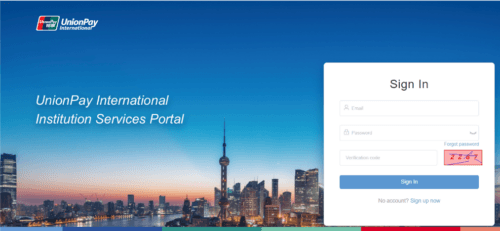

There are also several other options you may choose from on this page. If you select the second dot (shown in the picture below), you’ll be able to sign up for UnionPay’s service portal.

The sixth dot will allow you to integrate Apple Pay with UnionPay. More information on this can be found here.

Method Two → Stripe

As with Alipay and WeChat Pay, it’s often possible to enable UnionPay payments on your website via Stripe, and this means you do not need to create your own WeChat Pay account.

Other Chinese Online Payment Apps

For this next section, I will not go into as much detail because the apps in question are not as big as the ones mentioned already. I thought it would be a good idea to provide some insight into them anyway.

99Bill (快钱支付)

99Bill is a lesser-known electronic payment service in China.

The company is headquartered in Shanghai and also has offices in Beijing, Guangzhou, Shenzhen, and Nanjing.

According to their website, they have “established strategic partnerships with over 50 banks and financial institutions in China. In addition, the company also supports payment via major international cards, such as VISA and MasterCard. The company’s services currently cover a total of 3 billion domestic and international bank cards.”

Below are just a few of 99Bill’s collaborators.

In addition to payment processing, 99Bill offers features like account recharge and withdrawal, enabling users to easily manage funds for online transactions.

The platform also offers a batch payment function for corporate users, facilitating the handling of multiple transactions efficiently.

For marketing and customer retention, 99Bill provides a coupon system that benefits both users and merchants by offering discounts and promotions.

Additionally, it includes personal services like utility bill payments, credit card repayments, and mobile phone top-ups, enhancing everyday convenience for its users.

99Bill was bought by the search engine and AI company Baidu in 2014 and is currently sitting in sixth place this year (moving up three spots since 2022).

壹钱包 (One Wallet)

Belonging to Ping An Insurance, One Wallet is dedicated to providing a diverse range of third-party payment services for individual consumers and corporate clients, including internet and mobile payments.

It aims to offer innovative Internet financial and consumer services that encompass wealth management, protection, lifestyle, and consumption, hoping to create value for every penny through an electronic wallet account.

An Active Wallet is a stable return cash appreciation service that allows users to yield a certain return after transferring money.

Essentially, users are purchasing a money market fund called “Daily Profit” provided by Ping An Great Wall Fund.

An initial purchase can begin as low as 1 fen (roughly 0.0014 USD), any funds kept in this wallet can be withdrawn to a card, and T + 0 immediate settlement is supported.

Funds will be transferred very quickly (sometimes as fast as a minute), and this wallet can be used at any business with One Wallet.

One Wallet Capricious Wealth Management is a service for loan debt transfers.

A consigned load creditor can transfer loan assets to a debt assignee through the One Wallet App.

The company promises flexible and high returns as well as low risk (1000 CNY is the minimum allowed purchase).

拉卡拉 (Lakala)

Established in 2005, Lakala’s online payment services come in eighth place (a position it has held since 2022).

As a subsidiary of Lenovo and the largest offline e-payment company in China, Lakala is headquartered in Beijing and has 25 branches nationwide.

Lakala’s overseas subsidiary, Lakala International, was established in 2019 in Hong Kong.

The company promises its customers the ability to settle cross-border funds 24/7 with zero currency conversion loss and no fee for RMB withdrawals.

Outside of its online services, Lakala is also in the business of payment kiosks and has over 30,000 in convenience stores and supermarkets in 30 Chinese cities.

汇付天下 (Huifu Payment Limited)

Established in 2007 in Shanghai, Huifu Payment was the first digital payment firm to try to go public by listing in Hong Kong in 2021, but that attempt unfortunately failed.

Like Alipay and WeChat, Huifu provides fintech technology related to data and account management to businesses. However, the company has tried to differentiate itself by focusing on payment services for micro and small merchants.

Huifu announced this year it was upgrading its payment services to be cloud-based, and its new Dougong 2.0 has been made with cross-border businesses and small businesses in mind.

These enterprises usually prefer payments by the number of transactions instead of a complete package.

Huifu believes that by offering tailored services to bigger companies and cheaper services to small companies, it can rival Alipay and WeChat.

Huifu is doing this because it wants to take advantage of all the Chinese companies going abroad. It is already serving SHEIN, a Chinese fast fashion brand that has become very popular in North America in recent years due to its cheap but nice-looking outfits.

Understanding AliPay and WeChat Pay’s dominance in China’s major cities, Huifu concentrates on smaller companies in second and third-tier cities. ?

Recently, Standard Chartered signed a deal stating that it would provide financial services to Huifu for cross-border e-commerce companies in ASEAN, the Middle East, and countries involved with the Belt and Road Initiative, China’s global infrastructure diplomacy initiative.

Despite Huifu’s small presence compared to WeChat Pay and Alipay, this partnership seems a big deal as Standard Chartered operates in 64 countries and shares almost 75% of its worldwide footprint with the Belt and Road Initiative.

Their website can be found here.

Below are some of Huifu’s collaborators.

Despite Huifu’s achievements, it has slipped to ninth place, down two from 2022.

Yeepay

Established in 2003, Yeepay is headquartered in Beijing and has more than 30 branches across China, was one of the first payment companies to obtain a payment license from the People’s Bank of China in 2011.

They have served more than a million merchants and received over 200 awards, including an Excellent Cross-Border E-commerce Financial Enterprises reward in 2020.

Earlier in 2024, Yeepay met with major airlines, hotels, OTAs, DMCs, TMCs, travel technology providers, and tourism enterprises in Berlin to discuss business collaboration.

Among the airlines it met were Lufthansa Innovation Hub, Omio, Traffics, and TUI Group.

Yeepay is already accepted by every airline in China and has partnered with more than 10,000 Chinese online travel agencies.

Like Huifu, Yeepay seems to be eyeing Chinese companies going global, and it recently teamed up with Singapore’s Sunrate to do just that.

Yeepay seems to have retained its 10th-place spot since 2022.

JDPay

JD.com has become well-known outside of China for going public on the US stock market.

However, it doesn’t seem to have an English website yet for its JDPay, despite being ranked as a Fortune 500 company.

JDPay offers a range of payment methods catering to various consumer needs, including

- card payments, Bai Tiao (a credit installment service),

- Xiao Jin Ku (a money market fund),

- innovative solutions like JD Flash Pay, and

- face recognition payment.

Card payments allow verified users to link their bank cards for online and offline transactions.

Bai Tiao, launched in February 2014 by JD Finance, another arm of JD.com, provides a “buy now, pay later” service with options for interest-free periods and installments ranging from 3–24 months.

Xiao Jin Ku combines shopping payments, cash management, and investment, enabling instant transactions without external gateways.

JD Steel Pellet, a type of loyalty point, supplements these by allowing the conversion of points earned elsewhere into discounts at JD Mall.

JD Flash Pay, leveraging NFC technology via a UnionPay collaboration, offers a secure and convenient payment experience across millions of point-of-sale terminals.

Introduced in August 2017, face recognition payment uses live detection and anti-spoofing technologies to ensure high security and efficiency in identity verification across various applications, including vending machines.

Although Chinapp, the Chinese source I used for rankings, did not include JDPay, we can see from China Daily’s 2022 article that JDPay has moved up from fifth place in the past two years.

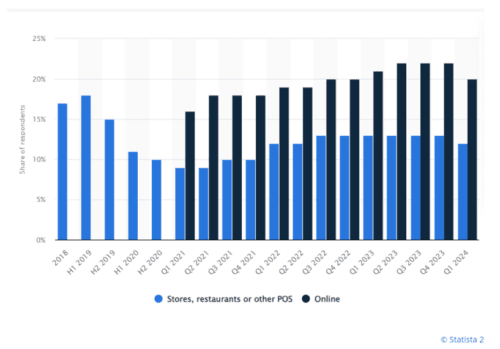

Apple Pay

Apple Pay has been available in China since 2016.

As a company, Apple needs no real introduction, but what relationship do Chinese consumers have with its payment app?

As you can see from the above, the company has lost market share in terms of its usage in stores and restaurants, while its usage online has remained consistent.

According to Techwire, most retailers in China chose to stick with WeChat and Alipay.

Even Apple’s partnership with UnionPay did not change this. Techwire points out:

“The simple fact is that using Apple Pay would result in more costly in-app transaction fees for consumers and higher equipment costs for merchants who would have to obtain specialized communication devices to run it.

Alipay and WeChat Pay use codes that can be scanned online or in person, making them the cheaper and simpler option. They also enable users to split bills or send money to each other, making it more appealing than Apple’s simplistic payments system.”

Another headache for the company is that Apple Pay only works on Apple phones.

In a country where local Android phones are getting more competitive every year, especially within the context of US-China relations, this problem won’t be solved any time soon.

Still, with Apple’s brand successes in China and Apple Pay’s ability to be used on the different products the company creates, one shouldn’t rule out the company’s competitive edge just yet.

According to Baidu, Apple Pay in China supports a total of 32 banks issuing debit and credit cards.

Bestpay (翼支付)

Based in Beijing, Bestpay is a third-party service platform owned by Tianyi E-commerce Co., Ltd, a subsidiary of China Telecom.

In 2011, it received a third-party payment license from the People’s Bank of China and has been cooperating and exploring interoperability with China UnionPay.

It also recognizes QR code payments in collaboration with UnionPay QuickPass, Alipay, and WeChat Pay.

Bestpay serves 70 million monthly active users, offering services such as public utility payments, consumer shopping, and financial management.

It relies on technologies like cloud computing, big data, and artificial intelligence, working together with partners to empower over 10 million offline merchant stores and more than 170 well-known online e-commerce platforms.

Bestpay has introduced measures to reduce operational costs for small and micro-businesses, including waiving payment account withdrawal fees for three years starting September 30, 2021, and providing discounts on online payment fees for eligible small and micro-enterprises, with extra incentives for those involved in rural revitalization.

Additionally, at its fifth annual partner conference, Bestpay launched the “Merchant Gold Card 2.0,” a comprehensive solution combining telecommunications, cashier services, and customer acquisition to support smart business management.

This upgraded service leverages China Telecom’s network and Bestpay’s payment capabilities to offer hardware and comprehensive online management services, while promoting efficient traffic generation for stores through high-quality online traffic and marketing activities.

PayPal

PayPal, like Apple, doesn’t need an introduction.

In 2021, the company became the first foreign firm to have a 100% stake in a payments platform. PayPal previously had also acquired a 30% stake in the Chinese payment platform GoPay.

As a leader in cross-border payments, PayPal has hoped to provide Chinese customers with the same capabilities and services as it does in other countries.

While 300,000 merchants in China use PayPal for their business, the company believes its use of AI technology to prevent fraud will give it an advantage over the competition.

SeekingAlpha believes that PayPay will play an increasing role in the future of e-commerce and cross-border transactions in China.

Huawei Pay

We previously mentioned Huawei’s relationship with other payment services.

The company has its own payment service as well.

This is important given the company’s success at competing with Apple in China and other countries where it’s accepted (according to Huawei’s website):,

- Russia,

- South Africa,

- Pakistan,

- Germany, and

- Austria.

However, in some of these countries, the service is only possible with QR codes.

More information on this can be found here, and Yahoo reports that Huawei Pay is also available in Hong Kong, Malaysia, Singapore, and Thailand.

Huawei works like every other service mentioned in this article, but in case you need more info, please check out this link. It offers both NFC and QR code payments for in-store purchases.

Fingerprint recognition, tokenization, and biometric authentication provide customers with privacy and security.

In Europe, Huawei has partnered with Curve, a financial app, to help customers pay using their phones.

One similarity between Huawei and a few other online payment services is it also works with UnionPay.

According to Yahoo! Finance, only 9.9% of Chinese users use Huawei Pay, but if the company can build up an ecosystem and branding like Apple has over the past 20 years, maybe it will grow its user base too.

Furthermore, Huawei is similar to Apple because the company produces other tech besides phones (e.g. smartwatches), which can also give them a competitive edge.

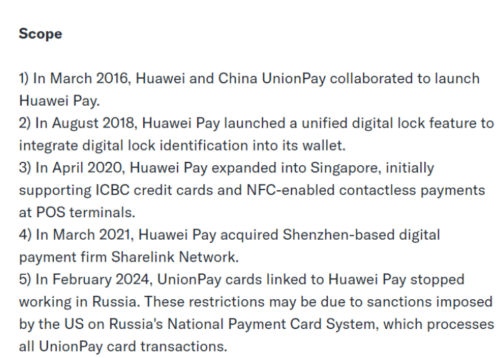

Below is a chart from Yahoo showing a timeline of Huawei Pay.

Baofu (宝付)

With 7% of China’s market, according to Statista, Baofu is not a strong competitor, but one nonetheless.

Baofu has a comprehensive business reach, covering over thirty industry sectors and servicing more than 20,000 enterprises and merchants.

With daily transaction volumes exceeding 30 million, Baofu’s global operations are well established.

Headquartered in Shanghai, the company has subsidiaries in major Chinese cities:

- Beijing,

- Shenzhen,

- Hangzhou,

- Guangzhou,

- Haikou, and

- Hong Kong.

Internationally, Baofu has offices in Singapore, the United States, Japan, and the Cayman Islands in the United Kingdom.

These global operations facilitate international business collaborations, enhancing Baofu’s worldwide strategic presence.

Its business can be broken down as follows:

- Internet Banking

- Baofu’s Internet banking system uses bank cards issued by major banks as the payment medium, allowing users to complete online transactions directly through the corresponding online bank.

- Top Ups

- Baofu’s card top-up system resolves small transaction payment issues between merchants and users. Users can simply enter the amount they wish to top up a card and a password without using a bank.

- Account Payments

- Baofu users can use a registered Baofu account as a virtual account for financial management. Services include online transactions, checking account balances, receiving payments, making payments, top-ups, and withdrawals.

- Express Payments

- Baofu’s express payment feature does not require any online bank account to be opened. Users can make online payments conveniently by entering information such as card numbers and passwords.

- Large Amount Payment

- Baofu provides a secure, efficient third-party payment platform for large B2B e-commerce transactions, such as online gaming. It supports unlimited payments from corporate bank accounts and large payments from personal cards, addressing merchant bottlenecks in large transactions. The platform facilitates single-step transactions and offers a “Baofu green channel” to speed up merchant capital turnover.

Mi Pay

Although Mi Pay is not considered a strong competitor, it deserves mentioning given Xiaomi’s strength in the international phone market, especially in the Global South.

If India hadn’t shut down the company’s apps a few years ago (along with many other Chinese apps), Mi Pay may be in a better place today.

Launched in 2018, Xiaomi also has partnered with UnionPay in China and uses an NFC-based mobile payment system that supports credit, debit, and public transportation cards in China.

Like Huawei and Apple, a range of Xiaomi products can be attached to Mi Pay.

As of now, 34 countries accept payment with Mi Pay.

Contact Us

China’s world of online payments is growing and changing every year.

For companies from countries where credit cards and money are the main forms of payment, the predominantly cash-less Chinese market may seem a little daunting.

But it doesn’t have to be.

Arrange a free consultation with us here to discuss the options available to you and your business.

For more information on Chinese marketing in general, there’s our China Digital Marketing 101 page.